By SVL (Store Vision Ltd)

- 1. Executive Summary: Regulatory Change in Ireland’s Impact Protection Sector

- 2. Introduction: The Irish Industrial Safety Landscape

- 3. Market Sizing & Segmentation

- 4. Economic Drivers & Market Dynamics

- 5. Regulatory & Compliance Landscape

- 6. Competitive Landscape Analysis

- 7. Digital Procurement & Search Landscape Analysis

- 8. Future Trends & Market Outlook

- 9. Strategic Implications for Irish Businesses

- 10. Conclusion: Market Maturity & Strategic Positioning

1. Executive Summary: Regulatory Change in Ireland’s Impact Protection Sector

As Ireland’s industrial, logistics, and manufacturing sectors enter a period of sustained, high-value expansion in early 2026, the industrial safety infrastructure and impact protection market has fundamentally transitioned from a reactive compliance requirement to a strategic operational investment. This comprehensive market analysis examines the critical forces shaping the Republic of Ireland’s impact protection sector, detailing the economic catalysts, regulatory pressures, and shifting competitive dynamics that define the current landscape.

The Irish impact protection market is experiencing a profound period of acceleration. Driven by a robust foreign direct investment (FDI) pipeline, the relentless expansion of the e-commerce logistics footprint, and escalating regulatory enforcement, the sector is maturing rapidly. Recent data from the Central Statistics Office (CSO) indicates a €35 billion construction market in 2025, with non-residential and industrial building showing continued annual growth. Correspondingly, demand for high-performance safety infrastructure – encompassing traffic management, pedestrian segregation, racking protection, and specialized wall cladding – has surged.

However, this growth is set against a deeply sobering regulatory backdrop. Following a historic low of 36 workplace fatalities in 2024, the Health and Safety Authority (HSA) reported a dramatic 61% surge to 58 work-related fatalities in 2025. Crucially, incidents involving being struck by a vehicle (14 fatalities) and heavy/falling objects (14 fatalities) constituted nearly half of these tragedies. This severe spike has triggered an era of unprecedented HSA enforcement rigor, fundamentally altering procurement priorities from “minimum viable compliance” to absolute, verifiable infrastructure resilience.

Key strategic insights from this analysis include:

- Economic Catalysts: Record-breaking FDI in 2025 – including 323 project announcements and massive capital expenditure in the pharmaceutical and med-tech sectors (such as significant expansions in Cork, Kerry, and Dublin) – is driving demand for GMP-compliant, high-specification impact protection.

- Regulatory Intensification: The HSA’s pivot toward evidence-led, sector-specific inspections in 2026, alongside stringent Food Safety Authority of Ireland (FSAI) hygiene audits, is compelling businesses to upgrade legacy infrastructure.

- Market Fragmentation & Consolidation: The supplier landscape remains fragmented, divided among comprehensive local specialists, niche providers, and UK/international entrants. However, the complexities of post-Brexit supply chains and localized regulatory demands heavily favor indigenous operators who offer turnkey, consultative expertise.

- Digital Procurement Evolution: Analysis of B2B search behavior reveals a maturing buyer journey. Facility managers are conducting extensive digital research on total cost of ownership (TCO) and compliance specifications before engaging suppliers, demanding transparent, authoritative market education.

For C-suite executives, facility directors, and health and safety officers, this intelligence provides a critical benchmarking tool. As thought leaders in the Irish market, SVL Store Vision presents this analysis not as a product catalog, but as an essential strategic framework. In an era where operational downtime, regulatory fines, and supply chain bottlenecks present severe business risks, understanding the macro-dynamics of the impact protection market is indispensable for safeguarding both human capital and corporate assets.

2. Introduction: The Irish Industrial Safety Landscape

The industrial safety landscape in the Republic of Ireland has reached a critical inflection point. No longer viewed as a peripheral facility expense, impact protection and infrastructure resilience are now recognized as core pillars of enterprise risk management, operational continuity, and corporate governance. This shift is deeply intertwined with Ireland’s broader economic trajectory and its unique position within the European and global supply chains.

The Macro-Economic Foundation

Ireland’s position as a premier European logistics hub and a global center of excellence for life sciences, technology, and advanced manufacturing has profoundly shaped its industrial footprint. The e-commerce revolution has not merely increased the volume of warehousing space; it has fundamentally altered the throughput velocity and operational intensity of these facilities. With distribution centers operating 24/7, the frequency of interactions between heavy material handling equipment (MHE) and pedestrian traffic has multiplied exponentially.

Concurrently, Ireland’s success in attracting Foreign Direct Investment (FDI) – spearheaded by IDA Ireland – has introduced rigorous multinational safety standards into the domestic market. In 2025, IDA-supported companies achieved record employment of over 312,000, with €2.5 billion spent on research, development, and innovation. The proliferation of high-value pharmaceutical manufacturing and data centers demands infrastructure that not only prevents physical damage but strictly adheres to Good Manufacturing Practices (GMP) and cleanroom protocols. This has elevated the specification requirements for protective barriers, bollards, and wall protection far beyond standard industrial applications.

The Evolving Regulatory Environment

The regulatory environment governing Irish workplaces is characterized by increasing stringency and a zero-tolerance approach to preventable accidents. The Health and Safety Authority (HSA) operates with a robust legal mandate under the Safety, Health and Welfare at Work Act 2005. Following the alarming 61% increase in workplace fatalities recorded in 2025, the HSA has signaled a shift toward highly targeted, risk-based inspections across high-risk sectors, particularly targeting workplace transport and working at height.

Furthermore, sector-specific bodies such as the Food Safety Authority of Ireland (FSAI) and the Health Information and Quality Authority (HIQA) enforce their own rigorous infrastructural mandates. For food and beverage processors, impact protection is inextricably linked to hygiene; damaged walls or barriers harbor bacteria and trigger immediate audit failures. Similarly, the integration of EU Directives – such as the Machinery Directive and rigorous CE marking requirements – ensures that the Irish market is legally bound to world-class safety hardware standards.

Compounding these domestic and European pressures is the ongoing structural reconfiguration of supply chains post-Brexit. The friction introduced into UK-ROI trade has accelerated the localization of supply chains, prompting Irish facility managers to source critical safety infrastructure from indigenous or EU-based suppliers to circumvent customs delays and cost volatility.

Market Maturity and the Professionalization of Safety

Historically, investment in impact protection in Ireland was heavily reactive – budget was allocated only after a catastrophic forklift collision, a failed audit, or an HSA improvement notice. Today, the market exhibits advanced maturity. The professionalization of the Environmental, Health, and Safety (EHS) function within Irish enterprises means procurement is increasingly proactive and data-driven. Buyers are deploying sophisticated cost-benefit analyses, recognizing that a €50,000 investment in robust racking protection and traffic management systems generates massive ROI by preventing €500,000 in operational downtime, inventory loss, and liability claims.

The Strategic Value of Market Intelligence

For decision-makers navigating this complex ecosystem, superficial product knowledge is insufficient. Procurement directors need to benchmark their infrastructural spending against macro-industry trends. EHS officers require deep foresight into HSA enforcement patterns. Operations directors must understand how macroeconomic variables – from construction inflation to logistics automation – will impact their facility expansion plans. This report bridges the intelligence gap, providing the data-backed clarity required to transition impact protection from a mandatory compliance burden into a definitive competitive advantage.

3. Market Sizing & Segmentation

Accurately quantifying the Irish impact protection market requires a nuanced synthesis of construction output data, facility density metrics, and sectoral investment patterns. Unlike standard commodities, safety infrastructure scales directly with the square footage of industrial real estate, the velocity of material handling, and the stringency of sector-specific regulations.

3.1 Total Addressable Market (TAM) Estimation

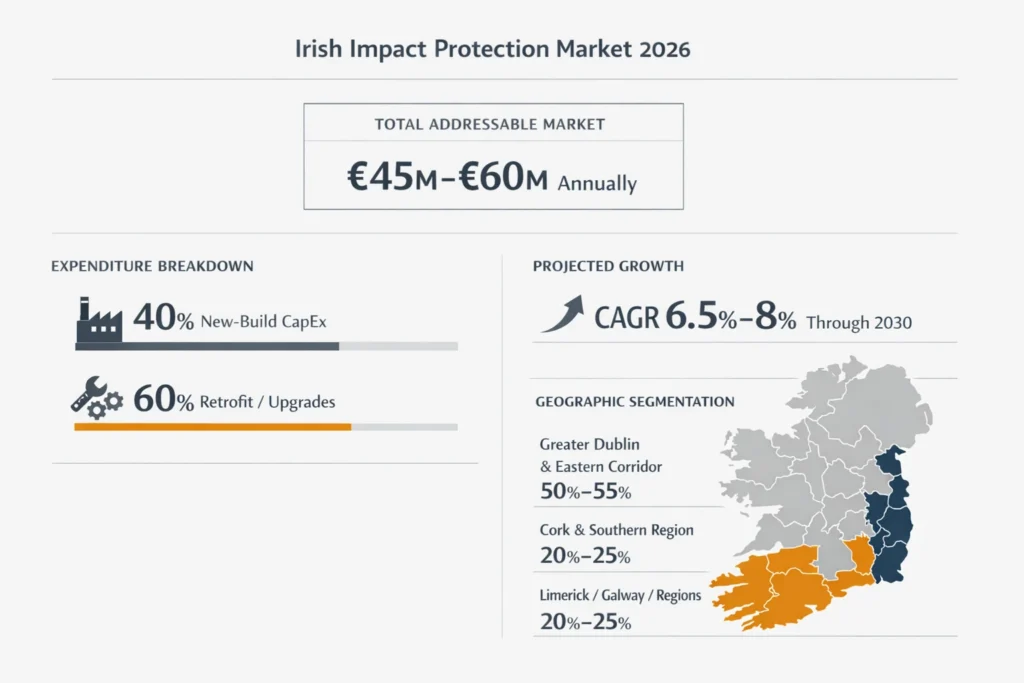

Based on primary economic indicators – including the CSO’s 2025 construction output reports, enterprise census data, and commercial real estate trajectories – the total addressable market (TAM) for impact protection and industrial safety infrastructure in the Republic of Ireland is currently estimated between €45 million and €60 million annually.

Methodology and Growth Dynamics:

New Construction vs. Retrofit: The market is bifurcated. Approximately 40% of expenditure is tied to new-build capital expenditure (CapEx), driven by the CSO’s reported 3.3% annual increase in non-residential building volume in Q4 2025. The remaining 60% is generated by the retrofit, replacement, and compliance-upgrade market across Ireland’s existing stock of thousands of warehouses, retail units, and manufacturing plants.

Average Facility Spend: Investment scales drastically by footprint and risk profile. A small 5,000 sq ft logistics hub may require a €3,000-€8,000 baseline investment in essential bollards and pedestrian barriers. Conversely, a 100,000 sq ft, high-throughput e-commerce distribution center or a GMP-compliant pharmaceutical facility will command an infrastructural safety investment of €100,000 to €250,000+, supplemented by €10,000 in annual lifecycle maintenance.

Projected CAGR: Benefiting from compounding drivers – industrial real estate expansion, regulatory pressure, and supply chain localization – the market is projected to experience a Compound Annual Growth Rate (CAGR) of 6.5% to 8% through 2030, outpacing general construction growth.

3.2 Geographic Segmentation

The distribution of infrastructural investment in Ireland is heavily centralized around primary logistics arteries and FDI clusters.

Greater Dublin & The Eastern Corridor (50-55% of Market Share): Unsurprisingly, the Greater Dublin Area (GDA) dominates market demand. This density is fueled by massive logistics parks along the M50 corridor, national retail distribution centers, and the concentration of corporate headquarters. The buyer profile here is highly sophisticated, intensely competitive, and driven by the rapid throughput demands of last-mile e-commerce delivery.

Cork & The Southern Region (20-25% of Market Share): Cork represents the highest-value segment per square meter, largely due to its status as a global pharmaceutical and life sciences hub. Recent investments, such as GE HealthCare’s €132 million facility upgrade in Cork, dictate demand for premium, ultra-hygienic, and chemical-resistant impact protection. The presence of the Port of Cork also sustains steady demand for heavy-duty marine and logistics barriers.

Limerick, Galway, and the Regions (20-25% of Market Share): The Mid-West and West are experiencing accelerated growth, aligned with IDA Ireland’s mandate for regional development (which saw 57% of FDI investments land outside Dublin in 2025). Galway’s med-tech cluster and Limerick’s advanced manufacturing parks require highly customized, specialized protective systems. Additionally, the border regions maintain unique cross-border logistics facilities that require robust infrastructure to handle heavy, fluctuating freight volumes.

3.3 Sector Segmentation Deep-Dive

To fully grasp the dynamics of the Irish market, we must dissect demand across five primary economic pillars.

Logistics & Warehousing (35-40% of Market)

- The Landscape: Encompassing 3PLs (Third-Party Logistics), dedicated brand distribution centers, cross-docking facilities, and last-mile depots.

- Safety Challenges: This sector represents the frontline of the HSA’s focus on workplace transport. High-speed forklift traffic, congested loading bays, blind corners, and densely packed high-bay racking create extreme risk vectors. Over 1,000 non-fatal injuries occur annually in the broader transport and storage sector.

- Core Solutions: Heavy-duty racking protection, deeply anchored steel bollards, heavy-impact pedestrian segregation barriers, and dynamic traffic management systems.

- Growth Trajectory: HIGH. Driven by the insatiable growth of e-commerce and the necessity to optimize vertical storage space, pushing racking higher and making structural impacts more catastrophic.

Retail & Wholesale (20-25% of Market)

- The Landscape: National supermarket chains, massive hardware/DIY outlets, pharmacy chains, and wholesale cash-and-carries.

- Safety Challenges: The unique challenge of retail is the convergence of heavy commercial delivery vehicles, MHE (pallet trucks/forklifts), and the general public. Asset protection (preventing shopping carts from destroying refrigeration units) is also a major financial driver.

- Core Solutions: Loading bay safety systems, public-facing pedestrian barriers, stainless steel architectural bollards, corner guards, and hygienic wall protection systems in back-of-house areas.

- Growth Trajectory: MEDIUM. Highly stable, driven by continuous store refits, expansion of discount supermarket footprints, and stringent public liability insurance requirements.

Food & Beverage Processing (15-20% of Market)

- The Landscape: From artisan indigenous producers and commercial kitchens to massive dairy processors, breweries, and meat export plants.

- Safety Challenges: A dual-threat environment. Facilities must withstand the heavy impact of pallet trucks moving heavy liquid/bulk loads while maintaining absolute clinical hygiene. Cracks in walls or rusted barriers lead to microbial harboring and catastrophic FSAI audit failures.

- Core Solutions: Food-grade hygienic wall cladding, high-density polyethylene (HDPE) barriers, stainless steel bollards, and easily washable, non-porous corner protection.

- Growth Trajectory: MEDIUM to HIGH. Driven by Ireland’s massive agri-food export market, which demands pristine, globally audited production facilities.

Pharmaceutical & Healthcare (10-15% of Market)

- The Landscape: Biopharma manufacturing plants, medical device cleanrooms, primary care centers, and national hospitals.

- Safety Challenges: Contamination control is paramount. Impact protection must not shed particles, must resist harsh chemical washdowns, and cannot obstruct critical airflow dynamics. In healthcare, impact systems must protect walls from hospital beds and catering carts while aiding infection control.

- Core Solutions: GMP-compliant cleanroom barriers, anti-microbial wall protection systems, flush-mounted corner guards, and specialized protective kerbing.

- Growth Trajectory: HIGH. Fueled by an unprecedented surge in life sciences FDI and increased governmental spending on healthcare infrastructure.

General Manufacturing & Industrial (10-15% of Market)

- The Landscape: Metal fabrication, electronics assembly, timber processing, and general engineering.

- Safety Challenges: Diverse and unpredictable. Mixed pedestrian and heavy machinery zones, overhead crane operations, and legacy building constraints.

- Core Solutions: Standard industrial barriers, machine guarding, highly visible floor demarcations, and column protectors.

- Growth Trajectory: MEDIUM. Steady, sustained by ongoing HSA compliance campaigns targeting machine safety and forklift operations.

4. Economic Drivers & Market Dynamics

The surge in demand for sophisticated safety infrastructure in Ireland is not occurring in a vacuum. It is the downstream result of several massive macroeconomic and structural shifts currently reshaping the Irish economy.

4.1 The E-Commerce & Logistics Revolution

Ireland’s integration into the global digital economy has revolutionized its industrial real estate landscape. The pivot from traditional brick-and-mortar retail to omnichannel distribution has drastically increased the demand for “big box” warehousing.

Impact on Safety Infrastructure:

- Throughput Velocity: Modern fulfillment centers operate with a throughput velocity that is magnitudes higher than traditional warehouses. More pallets moving per hour equals a statistically higher probability of collision.

- Downtime Intolerance: In an era of next-day delivery promises, taking a warehouse aisle offline for a week to repair a collapsed rack or a damaged wall is commercially devastating. Impact protection is increasingly viewed as an “uptime insurance policy.”

- Automation Integration: The rise of Automated Guided Vehicles (AGVs) and robotics requires specific safety infrastructure. While AGVs have sensors, the physical segregation of human workers from automated zones using rigid barrier systems remains a fundamental safety requirement.

4.2 Foreign Direct Investment (FDI) & Advanced Manufacturing

IDA Ireland’s 2025 results confirmed a record-breaking 38% increase in FDI projects, firmly cementing Ireland as a global hub for life sciences and technology. Multinational corporations (MNCs) do not adopt local safety minimums; they import their global corporate safety standards, which routinely exceed domestic legal requirements.

Market Implications:

- The “Gold Standard” Effect: When an American biopharma giant builds a facility in Cork with cutting-edge, polymer-based, hygienic impact barriers, it creates a new benchmark. Local contractors, facility managers, and even indigenous supply chain partners are subsequently pressured to elevate their own infrastructural standards to maintain contracts with these MNCs.

- First-Time CapEx: The sheer volume of new greenfield manufacturing sites results in massive, first-time, comprehensive safety installations, transitioning market volume from piecemeal retrofits to holistic facility fit-outs.

4.3 Regulatory Enforcement & The Cost of Non-Compliance

Economic drivers are heavily reinforced by the punitive costs of non-compliance. The HSA’s provisional data for 2025 revealed 58 workplace fatalities – a deeply concerning 61% increase from 2024. Consequently, the HSA’s mandate for 2026 involves aggressive, evidence-led workplace inspections.

The Financial Calculus of Safety:

- Direct Penalties: HSA prosecutions can result in massive corporate fines. Recent years have seen construction and manufacturing firms fined anywhere from €50,000 to €175,000+ for serious breaches involving workplace transport and lack of risk assessment.

- Insurance Premiums: The Irish liability insurance market remains exceptionally tight. Facilities lacking documented, high-grade physical impact protection face exponentially higher premiums. Conversely, businesses that proactively install verifiable safety infrastructure can negotiate stabilized or reduced premium rates.

- Litigation and Settlement: The cost of an employee injury claim (medical, lost time, legal fees, settlement) resulting from inadequate pedestrian segregation vastly outweighs the capital expenditure required to install a comprehensive barrier system.

4.4 The Construction Boom & Industrial Real Estate

Despite inflation and supply-chain volatility, the Irish construction sector remains robust. The CSO reported a total market value approaching €35 billion in 2025, with non-residential building output maintaining steady growth.

Market Implications:

- Early-Stage Specification: In modern industrial construction, impact protection is no longer an afterthought bolted on just before handover. Architects and engineering firms are actively specifying safety infrastructure – such as core-drilled bollards and integrated loading bay protection – during the blueprint phase.

- B2B2B Channels: This trend has elevated the importance of the contractor and developer channel. Safety infrastructure suppliers must now engage not just with the end-user, but with main contractors, requiring deep technical documentation (BIM models, CE certifications, fire ratings).

4.5 Brexit & Supply Chain Reconfiguration

The reverberations of Brexit continue to reshape procurement in Ireland. Prior to 2020, a significant portion of Ireland’s industrial safety equipment was imported “just-in-time” from UK-based manufacturers.

The Post-Brexit Reality:

- Friction and Delays: Customs declarations, rules of origin complexities, and transport delays have eroded the viability of relying solely on UK-based supply lines for time-critical facility fit-outs.

- The Localization Advantage: This structural shift provides a massive competitive advantage to indigenous Irish suppliers and those with deeply established EU supply chains. B2B buyers in Ireland are increasingly prioritizing local inventory, local installation expertise, and transparent, euro-denominated pricing without the threat of hidden import tariffs.

5. Regulatory & Compliance Landscape

To operate within the Irish impact protection market is to navigate a complex, multi-tiered framework of legal and regulatory obligations. Industrial safety infrastructure is not discretionary; it is heavily mandated by national law, European directives, and sector-specific authorities.

5.1 Health and Safety Authority (HSA) Framework

The HSA is the primary statutory body responsible for the enforcement of occupational health and safety in Ireland. The foundational legislation is the Safety, Health and Welfare at Work Act 2005, which places a strict duty of care on employers to provide a safe place of work, safe access and egress, and safe plant and machinery.

Workplace Transport Safety Guidelines: Given that vehicle-related incidents caused 14 fatalities in 2025, the HSA’s scrutiny of workplace transport is microscopic. The guidelines explicitly mandate:

- Pedestrian Segregation: A strict legal requirement to separate pedestrians from moving vehicles (forklifts, HGVs) using clearly defined routes and physical barriers. Yellow paint on the floor is increasingly deemed insufficient by inspectors; rigid, impact-resistant physical barriers are the expected standard.

- Racking Safety: Racking systems must be protected from vehicular impact. Damage to uprights compromises the structural integrity of the entire system, leading to catastrophic collapses. The installation of upright protectors and end-of-aisle barriers is standard enforcement protocol.

- Dynamic Risk Assessments: Employers must continuously update risk assessments reflecting changes in MHE traffic or facility layout, matching the grade of the physical protection to the weight and speed of the vehicles in operation.

5.2 Sector-Specific Regulatory Bodies

Beyond general HSA mandates, specific industries face rigorous, highly specialized audits.

Food Safety Authority of Ireland (FSAI): In the food and beverage sector, impact protection is fundamentally an issue of hygiene. Under strict EU and FSAI food hygiene regulations, facility surfaces must be maintained in a sound condition and be easy to clean and disinfect.

- The Compliance Threat: A forklift scratching a bare wall or denting a porous barrier creates microscopic crevices where Listeria or Salmonella can harbor. FSAI inspectors will issue immediate improvement notices or closure orders if infrastructural damage threatens food safety.

- The Solution: This mandates the use of food-grade, impact-resistant wall cladding, stainless steel bollards, and hygienic polymer barriers that do not rust, corrode, or chip upon impact.

Good Manufacturing Practice (GMP) for Pharmaceuticals: Ireland’s booming pharmaceutical sector operates under stringent GMP guidelines audited by the Health Products Regulatory Authority (HPRA) and international bodies like the FDA and EMA.

- Infrastructure within cleanrooms and production zones must be impact-resistant to prevent structural damage, but it must also be non-shedding, chemical resistant (to withstand aggressive sterilization procedures), and seamlessly integrated to prevent particulate accumulation.

5.3 European Union Directives and Standards

Irish safety regulations are deeply anchored in EU law.

The Machinery Directive (2006/42/EC): This directive governs the safety of powered equipment, including forklifts and automated logistics systems. It implicitly requires that the environment in which this machinery operates is physically equipped to manage the inherent risks, necessitating robust barrier systems.

CE Marking and Product Liability: The importation and sale of safety barriers and protective equipment in Ireland are governed by strict EU product safety frameworks. Quality impact protection systems must be rigorously tested and certified. Facility managers hold liability if they procure substandard, non-compliant safety hardware that subsequently fails during a collision, leading to injury. Consequently, comprehensive documentation, impact rating certifications, and technical data sheets are critical components of the modern procurement process.

5.4 Irish Building Regulations

The installation of physical infrastructure must not contravene national building codes.

- Part B (Fire Safety): Impact protection systems, particularly wall cladding and polymer barriers, must meet strict fire rating standards to ensure they do not contribute to flame spread or produce toxic smoke in enclosed warehouses. Furthermore, barriers must be strategically placed so as not to obstruct emergency egress routes.

- Part M (Access and Use): Pedestrian barriers and traffic management systems must be designed to accommodate wheelchair users and individuals with reduced mobility, dictating specific aisle widths and access gate mechanisms.

6. Competitive Landscape Analysis

The supply side of the Irish impact protection market is highly dynamic, characterized by a mix of historical incumbents, aggressive new entrants, and a growing divide between generic equipment suppliers and specialized, consultative solution providers. (Note: To maintain objective analytical integrity, this section categorizes the market without referencing specific competitor names).

6.1 Market Structure & Fragmentation

The Irish market exhibits moderate fragmentation. There is no single monopolistic entity controlling the majority of the market share. Instead, the ecosystem of approximately 15 to 25 active suppliers can be segmented into four distinct categories:

Category 1: Comprehensive Solution Providers (Market Share Estimate: 40-50%)

- Profile: Established, indigenous Irish companies operating as true consultative partners.

- Strengths: Deeply embedded local knowledge, extensive product portfolios covering everything from heavy-duty steel bollards to hygienic wall protection, and the ability to execute turnkey solutions (consultation, site survey, supply, and installation).

- Positioning: They dominate the mid-to-enterprise tier, appealing to buyers who value long-term infrastructure resilience, compliance expertise, and single-source accountability.

Category 2: Niche / Single-Category Specialists (Market Share Estimate: 20-30%)

- Profile: Companies whose entire business model revolves around a single product line, such as exclusive warehouse racking protectors or purely hygienic wall cladding installers.

- Strengths: Extreme technical depth within their specific vertical.

- Weaknesses: Facility managers undergoing complete site refits find it burdensome to manage multiple niche vendors, often preferring the consolidated approach of Category 1 suppliers.

Category 3: E-Commerce Catalog & General Industrial Suppliers (Market Share Estimate: 15-20%)

- Profile: Large, often UK or EU-based catalog distributors where safety barriers are just one of 10,000 general industrial items (alongside mops, shelving, and office chairs).

- Strengths: High digital visibility, rapid “click-to-buy” functionality, and aggressive pricing on high-volume commodity items.

- Weaknesses: Zero consultative capability, no installation services, and limited ability to provide custom safety engineering for complex facility hazards. They cater primarily to the reactive, low-budget, or small-scale buyer.

Category 4: Indirect Channels (Construction & Fit-out Contractors) (Market Share Estimate: 10-15%)

- Profile: Civil engineering and warehouse fit-out firms that source impact protection from manufacturers and bundle it into broader construction projects.

- Strengths: Embedded in the earliest stages of new builds.

- Weaknesses: Product knowledge is often superficial, and margins are heavily squeezed.

6.2 Competitive Differentiators and Strategic Positioning

In a market where steel and polymer ultimately serve the same basic physical function, how do leading suppliers differentiate themselves? Analysis of the market reveals four primary competitive vectors:

1. The “Turnkey” vs. “Drop-Ship” Divide: The most significant differentiator in the modern Irish market is the provision of integrated installation. Buyers are increasingly risk-averse; they do not want the liability of having their own untrained maintenance staff incorrectly bolt a high-impact crash barrier into a concrete floor. Suppliers who offer professional, insured, and certified installation services command significantly higher margins and win larger enterprise contracts compared to drop-ship e-commerce vendors.

2. Regulatory Expertise and Consultation: Market leaders have shifted their messaging from “We sell barriers” to “We solve HSA and FSAI compliance risks.” By conducting comprehensive site surveys, identifying blind spots, and engineering traffic management flows, top-tier suppliers elevate themselves from vendors to strategic safety advisors.

3. Material Agnosticism (Steel vs. Polymer): The market is currently engaged in a robust debate between traditional steel infrastructure and next-generation flexible polymer systems. Suppliers restricted to only one material type are at a strategic disadvantage. The most successful operators take a material-agnostic approach, specifying rigid steel where ultimate stopping power is required (e.g., loading bays) and flexible polymer where energy absorption and floor preservation are prioritized (e.g., forklift lanes).

4. Supply Chain Resilience and Localization: As noted in the Brexit analysis, the ability to guarantee stock availability in Ireland is a massive competitive weapon. Suppliers holding significant physical inventory in the Republic of Ireland can offer lead times of days, completely outmaneuvering UK-based competitors hampered by customs friction.

6.3 Strategic Gaps and Market Opportunities

Despite market maturation, several strategic gaps remain unexploited by the majority of suppliers:

- The Transparency Gap: Many suppliers still rely on antiquated “Request a Quote” models, masking pricing and specifications. Buyers, increasingly conditioned by B2C e-commerce transparency, experience severe friction with this model.

- The Educational Gap: There is a distinct lack of high-level, authoritative educational content in the Irish market. Most supplier websites are merely digital brochures. Suppliers that invest in deep, data-driven content – calculating ROI on safety investments, explaining building regulations, and translating HSA mandates – will capture the “awareness” stage of the buyer journey.

7. Digital Procurement & Search Landscape Analysis

The B2B procurement journey for industrial safety equipment in Ireland has digitized rapidly. Today, 80% of the B2B buying process – research, specification benchmarking, and vendor shortlisting – happens online before a buyer ever engages a sales representative. Understanding this digital search landscape is vital for grasping how market demand is expressed in real-time.

7.1 Search Intent Mapping and Buyer Behavior

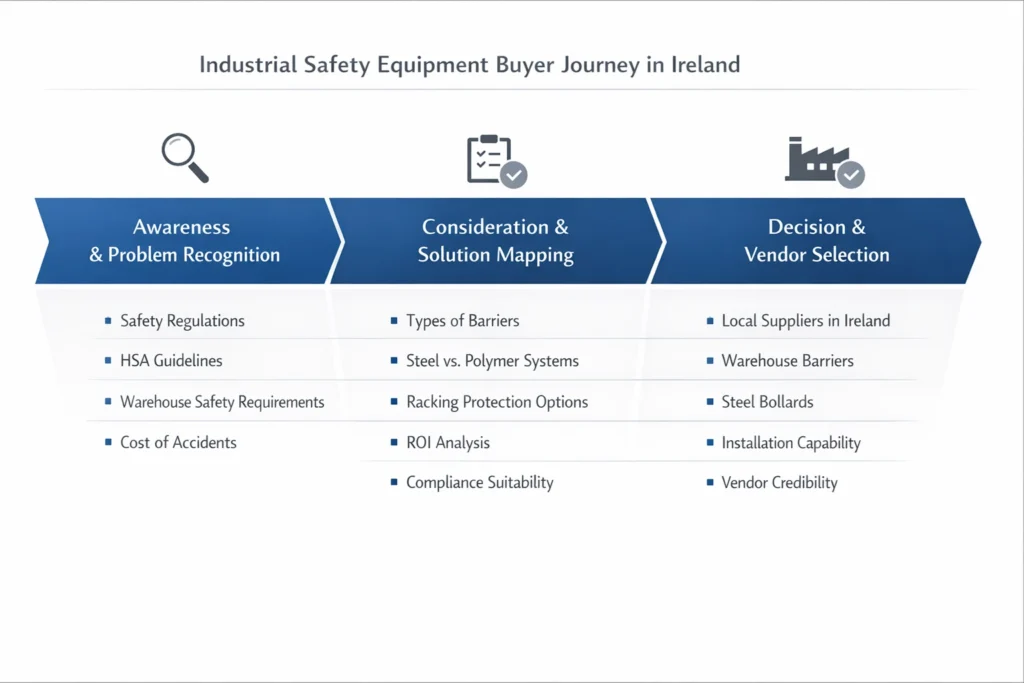

Irish facility managers and procurement officers utilize search engines in highly structured patterns, mapping perfectly to the classic procurement funnel:

1. The Awareness & Problem-Recognition Stage (Informational Intent) Triggered by an HSA inspection, a near-miss incident, or a new facility blueprint, buyers search for regulatory frameworks and macro-level guidance.

Indicative Queries: “HSA workplace transport guidelines,” “warehouse safety regulations Ireland,” “cost of warehouse accidents,” “FSAI wall protection requirements.”

Market Insight: Suppliers who provide robust, non-promotional answers to these queries establish profound early-stage trust. This is the domain of whitepapers, compliance checklists, and market analyses (such as this very document).

2. The Consideration & Solution-Mapping Stage (Commercial Investigation Intent) Having identified the regulatory need, buyers investigate infrastructural options, comparing materials, lifespans, and ROI.

- Indicative Queries: “impact protection market Ireland,” “types of warehouse barriers,” “difference between steel and plastic bollards,” “best racking protection systems,” “industrial safety equipment trends Ireland.”

- Market Insight: Here, the buyer is seeking technical authority. They are not yet ready to purchase; they are building the business case to present to their CFO. The market severely lacks robust total cost of ownership (TCO) calculators and material comparison guides.

3. The Decision & Vendor-Selection Stage (Transactional/Commercial Intent) The budget is approved; the specification is set. The buyer is now actively seeking localized suppliers capable of executing the project.

- Indicative Queries: “warehouse barriers Ireland,” “steel bollards Dublin,” “industrial safety equipment Ireland,” “buy racking protection Ireland,” “loading bay safety equipment.”

- Market Insight: These are high-value, highly competitive terms. Geographic modifiers (“Ireland,” “Dublin,” “Cork”) are explicitly used to filter out UK suppliers and ensure localization. Success here requires high-performance product landing pages backed by strong technical SEO, clear capability statements, and visible social proof (case studies, client rosters).

7.2 Keyword Prioritization and Demand Indicators

Analysis of the Irish search landscape reveals distinct tiers of market demand:

- Tier 1: High-Volume Core Infrastructure (The Bedrock) Queries surrounding “steel bollards Ireland” and “warehouse barriers Ireland” command the highest consistent search volumes. These represent the fundamental, non-negotiable elements of facility protection. Constant demand in this tier correlates directly with the ongoing expansion of the logistics and retail sectors.

- Tier 2: Broad Market & Supplier Discovery (The Macro View) Phrases like “industrial safety equipment Ireland” and “impact protection Ireland” serve as primary entry points for large-scale facility fit-outs. Buyers using these terms are generally looking for comprehensive, Category 1 suppliers capable of handling multi-faceted projects.

- Tier 3: Specialized, High-Value Long-Tail (The Niche Premium) While lower in raw search volume, queries such as “food processing wall protection Ireland” or “pharmaceutical warehouse compliance Ireland” carry extraordinarily high commercial value. These searchers have highly specific, heavily funded compliance mandates and are immune to budget-tier solutions.

7.3 The Strategic Imperative of Digital Authority

The analysis of the search landscape underscores a vital strategic reality: Digital visibility equates to market authority.

In a fragmented market, the supplier that dominates the informational and commercial investigation stages becomes the default specification standard. If a supplier’s proprietary guide on “HSA compliance for forklift segregation” is used by a facility manager to design their warehouse, that supplier’s products will inevitably be the ones specified in the final procurement tender. The Irish market is primed for a provider to aggressively seize this digital thought-leadership vacuum.

8. Future Trends & Market Outlook

The Irish impact protection market is not static. Over the next five years (2026–2030), a convergence of technological innovation, aggressive sustainability mandates, and evolving industrial architecture will fundamentally reshape how safety infrastructure is procured, deployed, and managed.

8.1 The Integration of Smart Safety Technologies (IoT)

The most disruptive trend entering the physical safety market is the digitalization of passive infrastructure. Impact protection is transitioning from “dumb iron” to “smart systems.”

Sensor Integration: Future barrier systems and bollards will be embedded with IoT (Internet of Things) accelerometers and strain gauges. When a forklift strikes a barrier, the system will instantly transmit an alert to the facility manager’s dashboard, logging the exact time, location, and force of the impact.

Predictive Maintenance: Currently, structural damage to racking or barriers is identified through manual, periodic inspections. Smart systems will facilitate predictive maintenance, notifying operators when a barrier’s structural integrity has been compromised before a secondary, catastrophic failure occurs.

Market Implication: This transitions the commercial model from a one-off CapEx product sale to an ongoing OpEx service model, heavily favoring technologically advanced suppliers who can offer “Safety Monitoring as a Service” (SMaaS).

8.2 Advanced Materials and Modular Engineering

While traditional steel remains essential for heavy-impact zones, the rapid evolution of polymer science is revolutionizing the broader market.

- High-Energy Absorption Polymers: Next-generation synthetics are engineered to absorb massive kinetic energy and flex upon impact, returning to their original shape. This protects the concrete substrate from being ripped up (a major hidden cost of steel barrier impacts) and reduces shock damage to the impacting vehicle and its driver.

- Modular Reconfigurability: Modern e-commerce warehouses are highly dynamic; layouts change seasonally. Modular barrier systems that can be rapidly unbolted, reconfigured, and redeployed without hot-works (welding) or specialized civil engineering are becoming the gold standard for agile logistics operators.

8.3 Sustainability and the Circular Economy

Ireland’s commitment to achieving ambitious climate targets is cascading down the industrial supply chain. Procurement departments are increasingly bound by strict Environmental, Social, and Governance (ESG) criteria.

- Decarbonization of Infrastructure: The production of heavy steel barriers is highly carbon-intensive. The market will see an aggressive shift toward solutions manufactured from highly durable, 100% recycled plastics and low-carbon extruded polymers.

- End-of-Life Management: Leading suppliers will differentiate themselves by offering “take-back” and recycling programs for damaged or obsolete barriers, ensuring zero waste to landfill and supporting the facility’s circular economy mandates.

- Market Implication: Sustainability is evolving from a “nice-to-have” marketing bullet point into a hard, heavily weighted metric in corporate procurement scorecards.

8.4 Aggressive Regulatory Evolution

The regulatory landscape will tighten progressively.

- Automation Safety Guidelines: As AGVs and robotics become ubiquitous in Irish warehouses, the HSA and EU bodies will issue specialized, highly stringent guidelines governing the interface zones where human workers and autonomous machines interact.

- Heightened Penalty Structures: In response to the high workplace fatality rates recorded in 2025, it is highly probable that the HSA will lobby for even more punitive financial penalties and direct director-level liabilities for gross negligence in infrastructure safety.

8.5 Market Consolidation

As the technical and regulatory demands of the market escalate, the barrier to entry will rise. Small, informal suppliers lacking CE certification, sophisticated digital capabilities, and dedicated installation teams will be squeezed out. We anticipate an era of consolidation, where larger, comprehensive solution providers acquire niche specialists to broaden their portfolios and dominate the enterprise space.

9. Strategic Implications for Irish Businesses

The macro-trends and data analyzed in this report carry profound strategic, financial, and operational implications for every tier of business leadership in Ireland. Recognizing impact protection as a strategic asset rather than a sunk cost is the defining characteristic of elite industrial operations.

9.1 For Facility Managers and Operations Directors

The operational velocity required to remain competitive in today’s logistics and manufacturing environment leaves zero margin for infrastructural downtime.

- Acknowledge the True Cost of Damage: An impact that destroys a €500 section of wall or a €1,000 piece of racking is not a €1,500 problem. If that damage forces the shutdown of a loading bay for 48 hours, or causes a refrigeration unit to lose temperature integrity, the true operational cost scales into the tens of thousands.

- Shift from Reactive to Proactive Investment: The era of patching holes and replacing bent steel after an accident is financially ruinous. Proactively hardening the facility with high-grade impact protection ensures operational continuity.

- Demand Turnkey Expertise: When selecting suppliers, prioritize those who offer comprehensive site surveys and installation. Utilizing internal maintenance staff to install high-liability safety infrastructure exposes the operation to severe risk if the installation fails during a collision.

9.2 For Health & Safety (EHS) Officers

The EHS function has never been under more intense regulatory scrutiny. Following the devastating 2025 fatality statistics, the HSA is operating with unprecedented vigilance.

- Documentation is the Ultimate Defense: A physical barrier is only half the solution; the documentation proving its certification, its appropriateness for the specific vehicle weight, and its maintenance log is what protects the company during an HSA audit or an insurance investigation.

- Sector-Specific Compliance: Recognize that generic solutions fail in specialized environments. An EHS officer in the food processing or pharmaceutical sector must ensure that the impact protection procured does not inadvertently violate FSAI hygiene rules or GMP cleanroom standards.

- Dynamic Risk Assessment: Traffic management is not “set and forget.” As facility throughput increases, risk vectors change. Continuous re-evaluation of pedestrian segregation effectiveness is a strict legal requirement.

9.3 For Procurement and Finance Teams

The procurement of safety infrastructure must transition from a “lowest-bidder” mentality to a Total Cost of Ownership (TCO) methodology.

- The TCO Calculus: Cheap, low-grade bollards or barriers may save 20% on initial CapEx, but they require constant replacement, destroy the concrete foundation upon impact, and cause severe damage to the MHE fleet. High-quality, energy-absorbing systems represent a vastly superior ROI over a 5-to-10-year lifecycle.

- Insurance Leverage: Proactive, heavily documented investments in premium impact protection should be actively utilized during annual liability insurance renewals to negotiate premium suppression.

- Supply Chain Risk Management: In the post-Brexit environment, finance teams should heavily weigh the hidden risks of importing infrastructure. Local, indigenous suppliers eliminate customs delays, remove currency fluctuation risk, and guarantee rapid mobilization for emergency repairs.

9.4 For Business Owners and the C-Suite

At the executive level, industrial safety is a matter of corporate governance, brand reputation, and enterprise valuation.

- Brand Protection: In sectors like food and pharmaceuticals, a hygiene breach caused by damaged facility infrastructure can trigger massive product recalls and devastating brand damage.

- Talent Acquisition and Retention: In a highly competitive Irish labor market, providing a visibly safe, highly organized, and professionally protected working environment is a crucial component of employee retention and morale.

- FDI and B2B Partnerships: If an indigenous Irish business wishes to integrate into the supply chains of the massive MNCs operating within the state, their facilities must mirror the world-class safety and infrastructural standards of those MNCs. Substandard facilities will fail vendor qualification audits.

10. Conclusion: Market Maturity & Strategic Positioning

The Republic of Ireland’s impact protection and industrial safety infrastructure market has definitively come of age. Fueled by a confluence of powerful economic drivers – a €35 billion construction sector, record-breaking FDI capital expenditure, and relentless e-commerce expansion – the demand for robust, compliant, and technologically advanced facility protection is accelerating rapidly.

However, this economic momentum is inextricably bound to a sobering regulatory reality. The tragic spike to 58 workplace fatalities in 2025 has galvanized the Health and Safety Authority, transforming robust pedestrian segregation and traffic management from a “best practice” recommendation into an uncompromising legal mandate. Simultaneously, stringent bodies like the FSAI and HPRA ensure that in Ireland’s high-value food and pharmaceutical sectors, infrastructural damage is synonymous with catastrophic audit failure.

In this high-stakes environment, the competitive dynamics of the supply chain heavily favor sophistication. The market is aggressively filtering out drop-ship catalog vendors and informal operators, elevating indigenous, comprehensive solution providers who combine deep regulatory knowledge with turnkey installation capabilities. Furthermore, the complexities of post-Brexit logistics have cemented the strategic necessity of localized, highly resilient Irish supply chains.

The Call to Strategic Action For Irish industrial, logistics, and manufacturing enterprises, the path forward is clear. Superficial compliance and reactive maintenance are no longer commercially viable strategies. The true cost of infrastructural failure – measured in operational downtime, inventory loss, surging insurance premiums, and HSA prosecutions – dwarfs the capital expenditure required to secure the facility.

As the market continues to evolve toward modular, sustainable, and IoT-enabled smart infrastructure, businesses must align with supply partners capable of delivering authoritative, consultative expertise. By benchmarking current safety infrastructure against the rigorous standards and macro-trends detailed in this analysis, Irish decision-makers can transition their impact protection from a mandatory overhead into a formidable engine of operational resilience and strategic competitive advantage.

In the modern Irish industrial landscape, securing the facility is synonymous with securing the future of the business.